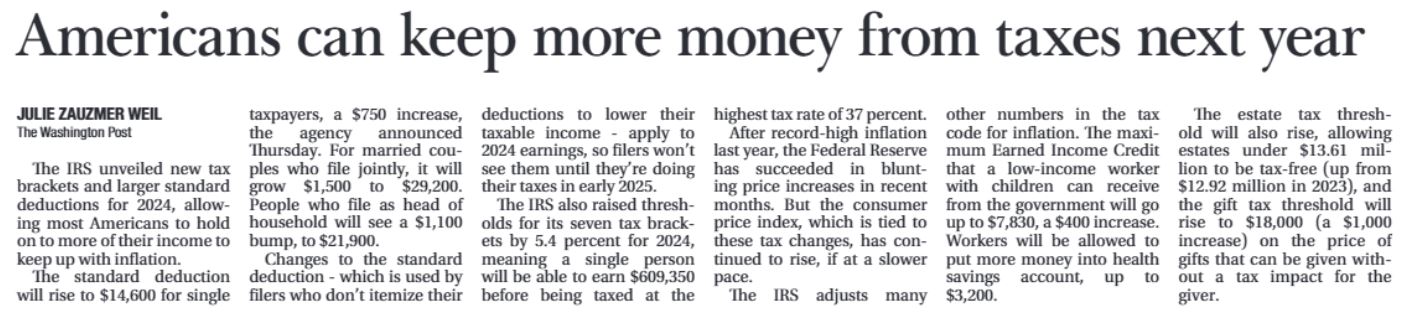

The new tax rates and brackets for 2024 were released by the Internal Revenue Service (IRS) on November 9, 2023. The new brackets reflect an inflation adjustment of 5.4%, which is lower than the 7.1% increase for 2023.

Here are the new tax rates and brackets for 2024:

Here are the new tax rates and brackets for 2024:

In addition to the changes to the tax brackets, the standard deduction is also increasing for 2024. For married couples filing jointly, the standard deduction will be $29,200, an increase of $1,500 from 2023. For single taxpayers and married individuals filing separately, the standard deduction will be $14,600 for 2024, an increase of $750 from 2023.

The changes to the tax brackets and standard deduction are expected to save taxpayers an average of $1,200 in 2024.

From the Daily Herald Sunday, November 19, 2023:

The changes to the tax brackets and standard deduction are expected to save taxpayers an average of $1,200 in 2024.

From the Daily Herald Sunday, November 19, 2023:

RSS Feed

RSS Feed