Choose a business structure

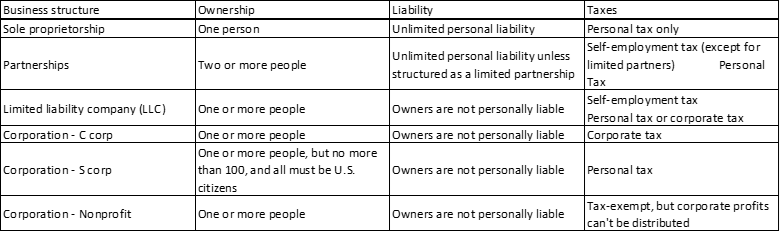

The business structure you choose influences everything from day-to-day operations, to taxes, to how much of your personal assets are at risk. You should choose a business structure that gives you the right balance of legal protections and benefits.

Your business structure affects how much you pay in taxes, your ability to raise money, the paperwork you need to file, and your personal liability.

Nonprofit corporation

Nonprofit corporations are organized to do charity, education, religious, literary, or scientific work. Because their work benefits the public, nonprofits can receive tax-exempt status, meaning they don't pay state or federal taxes income taxes on any profits it makes.

Nonprofit corporations need to follow organizational rules very similar to a regular C corp. They also need to follow special rules about what they do with any profits they earn. For example, they can't distribute profits to members or political campaigns.

Nonprofits are often called 501(c)(3) corporations — a reference to the section of the Internal Revenue Code that is most commonly used to grant tax-exempt status.

Certified B Corporations are businesses that meet the highest standards of verified social and environmental performance, public transparency, and legal accountability to balance profit and purpose. ... B Corps form a community of leaders and drive a global movement of people using business as a force for good.

While B Corp claims that certification balances the interests of shareholders with the interests of workers, customers, communities and the environment, B Corp standards are not legally enforceable. ... Certification is initially self-assessed, and doesn't override the profit-driven focus of the company.

What is the difference between a benefit corporation and a B Corporation?

The B Corp Certification is a third-party certification administered by the non-profit B Lab, based in part on a company's verified performance on the B Impact Assessment. The benefit corporation is a legal structure for a business, like an LLC or a corporation.

To qualify for a one-year term as a Pending B Corp, your company must:

Your business can apply for B Corp certification whether it's organized as a partnership, a limited liability company (LLC), or incorporated as a traditional C corporation. ... Startups can't earn B Corp status until they have been in business 12 months but they can apply for a certification-pending seal.

https://bcorporation.net/about-b-corps

The business structure you choose influences everything from day-to-day operations, to taxes, to how much of your personal assets are at risk. You should choose a business structure that gives you the right balance of legal protections and benefits.

Your business structure affects how much you pay in taxes, your ability to raise money, the paperwork you need to file, and your personal liability.

Nonprofit corporation

Nonprofit corporations are organized to do charity, education, religious, literary, or scientific work. Because their work benefits the public, nonprofits can receive tax-exempt status, meaning they don't pay state or federal taxes income taxes on any profits it makes.

Nonprofit corporations need to follow organizational rules very similar to a regular C corp. They also need to follow special rules about what they do with any profits they earn. For example, they can't distribute profits to members or political campaigns.

Nonprofits are often called 501(c)(3) corporations — a reference to the section of the Internal Revenue Code that is most commonly used to grant tax-exempt status.

Certified B Corporations are businesses that meet the highest standards of verified social and environmental performance, public transparency, and legal accountability to balance profit and purpose. ... B Corps form a community of leaders and drive a global movement of people using business as a force for good.

While B Corp claims that certification balances the interests of shareholders with the interests of workers, customers, communities and the environment, B Corp standards are not legally enforceable. ... Certification is initially self-assessed, and doesn't override the profit-driven focus of the company.

What is the difference between a benefit corporation and a B Corporation?

The B Corp Certification is a third-party certification administered by the non-profit B Lab, based in part on a company's verified performance on the B Impact Assessment. The benefit corporation is a legal structure for a business, like an LLC or a corporation.

To qualify for a one-year term as a Pending B Corp, your company must:

- Meet the legal accountability requirement for B Corp Certification. ...

- Complete and submit a prospective B Impact Assessment. ...

- Sign the Pending B Corp Agreement and pay a one-time fee of $500.

Your business can apply for B Corp certification whether it's organized as a partnership, a limited liability company (LLC), or incorporated as a traditional C corporation. ... Startups can't earn B Corp status until they have been in business 12 months but they can apply for a certification-pending seal.

https://bcorporation.net/about-b-corps

RSS Feed

RSS Feed